What Is an Irrevocable Life Insurance Trust?

An irrevocable life insurance trust — commonly called an ILIT — is a trust created specifically to own one or more life insurance policies on the grantor's life. The trust is both the owner and the named beneficiary of the policy. When the insured dies, the death benefit is paid to the trust — not to the insured's estate — and then distributed to the trust's beneficiaries according to the terms the grantor set when creating the trust.

The key word is irrevocable. Once created, the trust cannot be revoked or substantially modified by the grantor. The grantor cannot reclaim the policy, cannot change who the trust benefits, and cannot retain any control over how the trust operates. This permanence is what creates the tax benefit: by genuinely giving up ownership and control, the grantor removes the death benefit from the reach of the federal estate tax.

An ILIT is a specialized irrevocable trust — not a revocable living trust, not an AB trust, not a standard bypass trust. It is designed for one purpose: keeping life insurance proceeds outside the taxable estate while preserving the grantor's ability to direct where those proceeds ultimately go.

The Estate Tax Problem an ILIT Solves

Under Internal Revenue Code § 2042, life insurance death benefits are included in the insured's taxable estate if the insured held any "incident of ownership" in the policy at the time of death. Incidents of ownership include the right to:

- Change the beneficiary designation;

- Surrender or cancel the policy;

- Assign the policy to someone else;

- Borrow against the policy's cash value; or

- Revoke a prior assignment of the policy.

The practical implication is important and often surprises clients: a person who owns a $2 million life insurance policy and names their children as beneficiaries has done nothing to remove that $2 million from their taxable estate. The children receive the full death benefit — but the proceeds count toward the insured's estate for estate tax purposes. The estate tax is calculated on the larger estate, and the tax bill is paid from whatever assets remain.

This creates a particular problem for clients who purchased life insurance specifically to provide liquidity for estate taxes. A policy held inside the estate provides liquidity, but the death benefit itself makes the taxable estate larger — which makes the tax bill larger. The ILIT breaks this cycle. When the trust owns the policy, the death benefit does not increase the taxable estate, and the liquidity it provides is genuinely outside the tax calculation.

Utah has no state-level estate tax. Utah repealed its state estate tax effective January 1, 2005. Utah residents face only the federal estate tax, and an ILIT addresses only the federal calculation.

Who faces federal estate tax? The One Big Beautiful Bill, signed July 4, 2025, amended IRC § 2010(c)(3) to set the basic exclusion amount at $15,000,000 for calendar year 2026. A married couple can effectively shelter up to $30,000,000 through portability. Estates that exceed — or that may approach — those thresholds are the primary candidates for an ILIT. Life insurance death benefits count toward the total, so a large policy can push an otherwise-exempt estate into taxable territory.

How an ILIT Works: The Basic Mechanics

The standard ILIT structure follows a clear sequence:

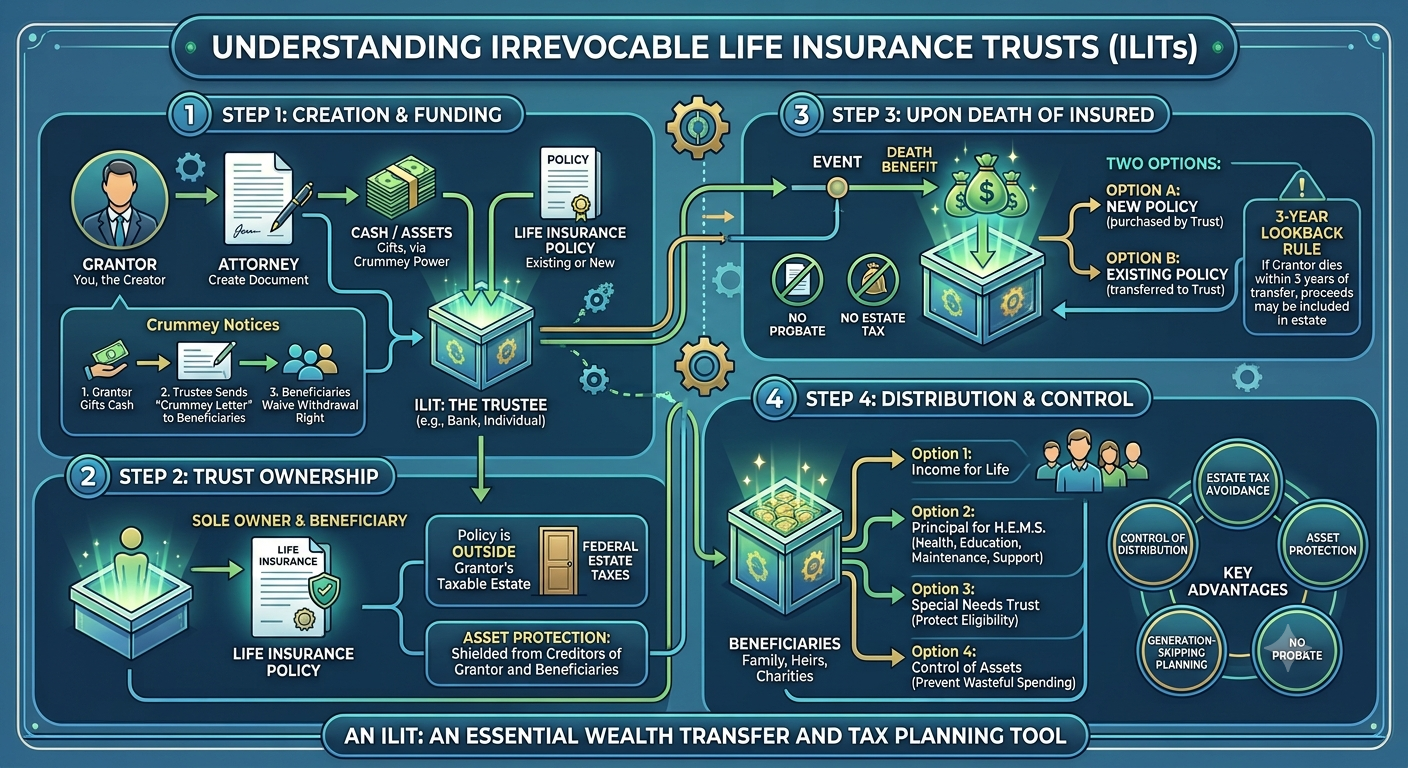

- Create the trust. An estate planning attorney drafts an irrevocable trust document. The grantor names a trustee — who must be someone other than the grantor — and the document defines who the beneficiaries are and how and when proceeds will be distributed after the grantor's death.

- The trust applies for and owns the policy. The trustee — not the grantor — applies for a new life insurance policy on the grantor's life. The trust is the owner from the first day the policy is in force. Because the trust is the original owner, the three-year estate inclusion rule (discussed below) never applies.

- The grantor makes annual cash gifts to the trust. The grantor contributes cash to the trust each year in an amount sufficient to cover the premium. These contributions are gifts for federal tax purposes.

- Crummey notices are sent. The trustee sends written notice to each beneficiary informing them that a contribution has been made and that they have a temporary right to withdraw their share. This step is what makes the annual gift qualify for the annual gift tax exclusion.

- The withdrawal right lapses and the premium is paid. If the beneficiaries do not exercise their withdrawal right within the stated window (typically 30 days), the right lapses and the trustee uses the contribution to pay the insurance premium.

- At death, the trust collects the death benefit. The death benefit is paid to the trust — not to the grantor's estate. The trustee then distributes the proceeds to the trust's beneficiaries according to the trust's distribution terms. The proceeds are excluded from the taxable estate and are generally income-tax-free to the beneficiaries under IRC § 101.

Example. A Utah business owner's wife passed away several years ago, and her estate tax exemption was fully used. He has a $13 million estate — business interests, real estate, and retirement accounts — and carries $3 million in life insurance naming his children as beneficiaries. His available federal estate tax exemption is $15 million. His total estate for federal estate tax purposes is $16 million — $1 million over the exemption. The federal estate tax on that $1 million excess is $400,000 at the 40% rate.

He creates an ILIT. The trust applies for a new $3 million policy on his life. He makes annual gifts to the trust to cover the premiums — the trustee sends Crummey notices to his children each year, and the children allow the withdrawal rights to lapse. He does not own the policy and has no incidents of ownership.

When he dies, the $3 million is paid to the ILIT — not to his estate. His taxable estate is $13 million, which is $2 million below the $15 million exemption. No federal estate tax is owed. The children receive the full $3 million from the trust, free of both income tax and estate tax, while the $13 million estate passes to them without estate tax as well. The ILIT converts a $400,000 tax bill into a $0 tax bill.

The Three-Year Rule: Why New Policies Beat Transfers

Many clients who learn about ILITs already own life insurance policies they want to move outside their estate. Transferring an existing policy to an ILIT creates a significant complication: under IRC § 2035, if the insured dies within three years of the transfer, the full death benefit is included in the taxable estate as though the transfer never happened.

The three-year rule is a statutory provision — it cannot be avoided by careful drafting or by structuring the transfer in a particular way. It applies to any transfer of an existing life insurance policy by the insured within three years of death.

The standard solution is to have the ILIT purchase a new policy from inception rather than transferring an existing policy. When the trust is the original applicant and owner, no transfer by the insured ever occurs, and IRC § 2035 does not apply regardless of how soon after forming the trust the grantor dies.

If an existing policy must be transferred — for example, because the policy has accumulated substantial cash value that the grantor does not want to surrender — the three-year clock starts running on the date of transfer, and the grantor simply must survive three years from that date for the proceeds to be excluded from the estate.

If you are in declining health, having the trust purchase a new policy may not be available to you. A new policy requires the insured to qualify medically, and deteriorating health can make that difficult or impossible. In that case, the planning conversation shifts: do you transfer the existing policy and hope to survive three years, or accept the estate inclusion and plan around it? This timing issue makes ILIT planning most effective when it is done well in advance of any health changes.

Crummey Powers: Making Annual Gifts to the ILIT Count

The grantor funds the ILIT by making cash contributions to pay premiums. These contributions are gifts. To minimize the gift tax cost of funding the trust, most grantors use the annual gift tax exclusion — $19,000 per recipient in 2026 — the amount that can be given to any individual each year without using any of the lifetime exemption and without filing a gift tax return.

The annual exclusion applies only to gifts of present interests — gifts the recipient can immediately use. A contribution to an irrevocable trust is normally a gift of a future interest because the beneficiaries cannot reach the trust assets right away. Future interest gifts do not qualify for the annual exclusion.

Crummey powers solve this problem. Named after the 1968 Ninth Circuit decision in Crummey v. Commissioner, the structure converts a future-interest gift into a present-interest gift by giving each beneficiary a temporary right to withdraw their allocable share of the contribution:

- Each beneficiary of the ILIT is given a temporary right — typically exercisable for 30 days — to withdraw an amount equal to the lesser of the annual exclusion or their pro-rata share of the contribution.

- The trustee sends a written Crummey notice to each beneficiary promptly after the contribution, notifying them of the deposit and their right to withdraw.

- If the beneficiary does not exercise the withdrawal right within the stated window, the right lapses.

- The trustee then pays the premium with the contribution.

Because each beneficiary had a genuine, unrestricted right to withdraw their share during the window, the IRS treats each contribution as a present-interest gift that qualifies for the annual exclusion.

The annual exclusion multiplies by the number of beneficiaries. A grantor with three adult children named as ILIT beneficiaries can contribute up to $57,000 per year (3 × $19,000) — one exclusion per Crummey power holder — without touching the lifetime exemption. Larger families can fund policies with higher annual premiums without gift tax cost.

Crummey notices are not a formality. The IRS has challenged ILITs where the withdrawal right was not real or where notices were never sent. Every notice must be in writing, must identify the amount available for withdrawal, must state when the right lapses, and must be sent promptly after each contribution. The trustee should maintain a documented record of every notice sent and every year the withdrawal right lapsed unexercised.

Choosing a Trustee

The grantor cannot serve as trustee of their own ILIT. If the grantor is the trustee, they retain control over trust assets — including the ability to cancel the policy, change the beneficiary, or assign the policy. These are incidents of ownership under IRC § 2042, and they bring the death benefit back into the taxable estate.

Common trustee choices include:

- An adult child or other family member. Suitable for straightforward trust terms and smaller policies. The trustee must be willing to actually fulfill the administrative obligations — sending Crummey notices on time, maintaining records, keeping the policy in good standing, and eventually distributing the death benefit.

- A trusted individual. A close friend, business partner, or other person with the judgment and availability to handle ongoing trustee responsibilities.

- A professional trustee or trust company. The right choice for large policies, complex distribution terms, or situations where a neutral professional is needed. Corporate trustees charge fees, but they also carry professional obligations and carry-through capability that individuals may not.

Selecting the wrong trustee is one of the most common ways ILITs fail in practice. The trust may be perfectly drafted, but if the trustee does not send Crummey notices, does not keep records, or allows the policy to lapse for nonpayment, the planning is undone. Whoever serves as trustee needs to understand the job and be prepared to do it consistently, year after year.

When Does an ILIT Make Sense?

An ILIT is not the right planning tool for every family with life insurance. It adds complexity — an irrevocable trust, a separate trustee, annual notices, ongoing administrative obligations — that is not warranted in every situation. An ILIT makes most sense in these circumstances:

- Estates that exceed or may approach the federal estate tax exemption. The primary purpose of an ILIT is to reduce the federal estate tax. For families well below the exemption threshold, the administrative overhead typically outweighs the benefit.

- Estates where life insurance was purchased specifically for estate tax liquidity. If the policy is intended to give heirs cash to pay the estate tax, holding it inside the estate defeats the purpose — the death benefit provides liquidity but simultaneously increases the estate tax bill it was meant to fund.

- Business owners with key-man insurance or buy-sell funding. An ILIT can own business-related policies, keeping the proceeds outside the owner's taxable estate while ensuring they reach the business or surviving owners as intended.

- Blended families. A surviving spouse and children from a prior marriage may have competing interests in a large insurance payout. An ILIT can direct proceeds directly to specific beneficiaries — including children from a prior marriage — without giving the surviving spouse access or control.

- Clients planning around potential estate tax law changes. Families with estates between a lower potential exemption and the current exemption may want to act while the current exemption levels are in place, rather than waiting for legislation that may reduce them.

Does your life insurance belong inside your estate?

If your estate may approach the federal estate tax threshold, the answer may be costing your family 40 cents on every dollar of death benefit. A free consultation can determine whether an ILIT makes sense for your situation.Limitations and Ongoing Obligations

Clients who proceed with an ILIT should understand its limitations before the trust is signed:

- The trust is irrevocable. Once created and funded, the grantor cannot change their mind, recover the policy, or significantly modify the trust terms. If family circumstances change — a divorce, the death of a beneficiary, a change of heart about who should benefit — the ILIT cannot be unwound.

- Crummey notices must be sent every year. This is an ongoing annual obligation. If the trustee stops sending notices, contributions to the trust no longer qualify for the annual exclusion, and the gift tax planning fails.

- The grantor cannot pay premiums directly. Premiums must be paid by the trustee from trust assets, not paid directly by the grantor to the insurance company. Direct payment by the grantor may be treated as an incident of ownership, particularly if the grantor retains a right to direct the payment. The correct structure is for the grantor to gift cash to the trust and the trustee to pay the insurer.

- Annual premium obligations are fixed. If premiums exceed the annual gift tax exclusion available (multiplied by the number of Crummey power holders), the excess must either be covered by the grantor's lifetime exemption or result in gift tax. Planning the policy size and premium structure around the available annual exclusions is part of the initial design.

- The three-year rule applies to transferred policies. If an existing policy is transferred and the grantor dies within three years, the estate inclusion applies regardless of the trust structure.

The ILIT and Generation-Skipping Planning

An ILIT can be structured as a generation-skipping trust by allocating generation-skipping transfer (GST) tax exemption to contributions made to the trust. When this is done correctly, the trust can continue for grandchildren — and potentially great-grandchildren — after the grantor's death, without triggering estate tax at the children's deaths.

This makes an ILIT a powerful tool for families who want to use life insurance proceeds not just to handle the current estate tax, but to build a fund that accumulates outside the estate tax system for multiple generations. The combination of the estate tax exclusion on death benefits and the GST exemption allocation can compound over time in ways that other structures cannot replicate.

GST planning inside an ILIT adds another layer of complexity and requires careful coordination with the attorney who handles both the trust drafting and the gift tax return that allocates GST exemption to the contributions. Done correctly, it is one of the more efficient multi-generational planning structures available.

Frequently Asked Questions

-

Naming a revocable living trust as beneficiary still leaves you as the policy owner. Ownership is what matters for estate tax purposes — under IRC § 2042, incidents of ownership at death trigger estate inclusion regardless of who is named as beneficiary. An ILIT works because the trust owns the policy from the start. The grantor has no ownership interest, no incidents of ownership, and no ability to change the beneficiary or borrow against the policy — and that is exactly what keeps the death benefit out of the taxable estate.

-

Crummey notices are written notifications sent to each ILIT beneficiary after a cash contribution is made to the trust. They inform the beneficiary that they have a temporary right — typically 30 days — to withdraw their allocable share of the contribution. This temporary withdrawal right converts the gift from a future interest (which does not qualify for the annual gift tax exclusion) into a present interest (which does). If notices are not sent, or if the withdrawal right is illusory, the IRS can treat the entire contribution as a future-interest gift that counts against the lifetime exemption rather than qualifying for the annual exclusion. Documented Crummey notices are one of the most important ongoing administrative requirements of an ILIT.

-

No. If the grantor serves as trustee, they retain control over the trust's assets — including the ability to change beneficiaries, cancel the policy, or assign it. These are incidents of ownership under IRC § 2042, and they pull the death benefit back into the taxable estate, eliminating the tax benefit the trust was designed to create. The trustee must be someone other than the grantor — typically an adult child, a trusted individual, or a professional trustee or trust company.

-

Under IRC § 2035, if you transfer an existing life insurance policy into an ILIT and die within three years of that transfer, the full death benefit is included in your taxable estate as though the transfer never happened. This three-year look-back cannot be avoided by trust drafting. The standard solution is to have the ILIT purchase a new policy from inception — when the trust is the original owner, no transfer has occurred, and the three-year rule does not apply.

-

No. Utah repealed its state estate tax effective January 1, 2005. Utah residents are subject only to the federal estate tax. An ILIT is designed to reduce federal estate tax on life insurance proceeds — it provides no additional benefit at the state level because Utah does not impose a state estate tax.